We Answer Your Biggest Questions

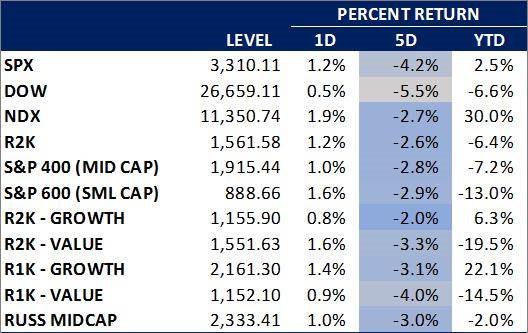

For anyone with money in the stock market the last month has been harrowing to say the least. The S&P 500 has tumbled more than 30% from its high in mid-February, oil prices have cratered, and the coronavirus pandemic threatens to cause economic chaos as businesses large and small shutter operations and furlough employees.

What should you do?

Inevitably there is concern about protecting your 401K and other retirement investments, no matter what your age or stage in life. Here we answer some of your biggest questions right now.

As someone who is three years out or less from retirement, what investments are safest to stay in? What investments should I stay away from?

For investors retiring with three years or less, your overall portfolio should be primarily invested in conservative vehicles such as bonds, hedge fund of funds and conservative stocks. When referring to bonds, think high-quality instead of junk bonds. A true hedge fund of fund, even though it has equities, should have much less risk than the S&P 500. For stocks, large cap dividend-oriented stocks would be the best strategies for general guidance. For more specific retirement plan advice, contact us at (203) 210-7814.

As a young investor, should I be moving my investments in my 401k to mostly bonds?

In the short term, moving money into bonds during uncertain times may be appropriate; however, then the decision will need to be made when to switch back to other investment vehicles. A more important question to address is to ask if investment decisions and allocations are based on your personal needs. Once that is determined, stick with a long-term approach. With a long-term outlook, your contributions are buying at lower prices, which inevitably will rise with a longer-term focus.

As an employer, what advice should I give my employees about how to manage their 401ks during this time?

As history tells us, impulsive decisions during market crises is counter-intuitive to the long-term approach of retirement planning. As an employer, there are many ways you can reassure your employees. They need access to direct advice, guidance and investment education on a regular basis, even more so during a time of stress. An employer should be working hand-in-hand with their financial advisor on frequent communications and ensuring there are a variety of ways to interact. An accessible advisor will help ensure every employee feels comfortable and informed versus scared and reactive.

For the aggressive investor, is this a stock buying opportunity?

If your allocation is weighted heavily in stocks, we would advise that you continue having your contributions go in at this lower pricing point. As the number of coronavirus cases increase, the resulting angst may continue to drive stock prices lower. However, this will not be forever. GGA believes the general indexes will be higher a year from now with the stimulus that has been injected into the market.

Can 401k contributions be temporarily stopped?

Any decision to stop contributions should be taken seriously. While it’s a personal decision, if you can afford it, do not stop. Contributions result in your ability to put tax-deferred dollars towards your retirement. If you want to stop because of the market volatility, an option would be to change your contributions to money markets. That way you are still contributing without taking risk. Just remember to switch your allocations back. All contributions should be based on individual needs to ensure your long-term approach is getting the results you expect.

How often should my allocations change in this type of market?

An allocation established through the Granite Group Advisors’ investment education toolkit should stay in place. History and experience tell us that markets go up and down in the short term, however; over the long-term, markets move up. While it may not happen overnight, remember that your current contributions are buying at lower price points. As the markets recover, that should help your retirement in years to come.

How do we know when the market is bouncing back?

It is very hard to catch a falling knife. One should instead look at forward indicators — one of the best is the Bullish Sentiment. At the moment the ratio is below 40%, which historically indicates investor sentiment is not optimistic at all and suggests one reason to buy. On the other hand, a 60% ratio means investors are extremely optimistic and stocks are likely overbought. We can’t emphasize enough that patience is a virtue in this market.

Given historical crises, how long will it take to reverse losses in my 401k?

In past bear markets, history has told us that the following year is typically an up year. While history has a way of repeating itself, there is no way to guarantee that this is certain. Still, Granite Group Advisors has no reason to believe as of today that it will be different this time. Depending on one’s allocation, time frame and how the markets behave, we expect to see a higher market return a year from now. The main takeaway: the markets will eventually come back and investors should be patient and hold their long-term view to see investment returns.